How the best financial plans are created

Predicting the future is always a perilous exercise. That is why any financial plan must make assumptions about the state of the world tomorrow. This includes inflation, the returns on your assets, etc.

When you go to the RetirePlan form, you answer several questions and then see your financial plan. What you don't see are the millions of calculations we perform in the background to optimise your investments, your insurance and your mortgages in order to optimise your financial situation according to your goals.

These calculations are based on two types of variables: (1) Facts that we know, such as your age and your income. (2) Estimates that we have to make, such as the future increase in the cost of living.

No adjustments

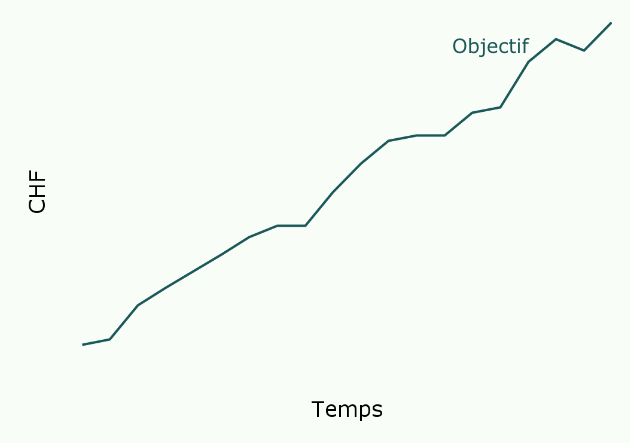

Regular adjustments

Until recently, financial planners relied on a mix of facts and estimates to draw up a plan for the rest of your life. The problem with this approach is that facts change and at least some of the estimates turn out to be wrong. The difference with RetirePlan is that we let you quickly update your plan whenever you want. We recommend doing so several times a year. These adjustments, small but regular, considerably increase the chances of reaching your goals.

This document will give you an overview of the facts and estimates we use to create your financial plan. If you have any questions - or even ideas for improving your financial plan - we would be delighted to hear them.

The basics

Every plan is unique, but there are certain basic assumptions that apply to almost everyone. Here are the main ones.

| Variable | Logic | |

|---|---|---|

| Annual inflation rate | 1% inflation on your expenses | The current situation in Switzerland is close to this rate of 0.5%. We update this rate periodically. |

| Interest rate on savings build-up | Weighted average | The interest rate we apply to savings build-up is a weighted average of all your investments. |

| Annual 3rd pillar transfer for employees | CHF 7'258 | Transferring the maximum annual amount into your 3rd pillar is always tax-advantageous as long as there is income. |

| Property maintenance costs | 1% of the property's value | As a property owner, in our financial projections we consider annual costs of a property equal to 1% of its market value. |

| Duration of a financial plan | 90 years | We assume a life expectancy of 90 years, based on FSO statistics, without distinction between men and women. |

| Mortgage: theoretical annual gross income required by the bank | 3 x ( 5% mortgage + 1% market value) | The following rule is the banking standard in Switzerland when calculating the income deemed acceptable for a mortgage. |

| Mortgage rate at maturity | 3% | At maturity, we automatically renew your mortgage loan and assign a rate of 3%. |

| Calculation of the tax burden | Taxes | We calculate taxes based on the data from the form and the tax brackets for the current year. This also applies to future taxes. |

| Pension fund contributions | Pension fund | We apply linear contributions to your pension fund between the current amount and the amount projected at retirement. In reality, your contributions vary depending on how your income and age develop. |

| Which cantons are covered by RetirePlan? | Cantonal tax calculations | We have modelled the taxation of all French-speaking cantons. For now, it is only possible to estimate the tax burden in the following cantons: Vaud, Geneva, Valais, Fribourg, Neuchâtel, and Jura. |

| How are taxes on the returns of taxable capital handled? | Calculation of income tax | We estimate that 5% of the returns on taxable capital count as income. |

| How is the market value of real estate defined? | 0.5% | The value of real estate changes over time. Based on historical data and taking a long-term perspective, our model predicts an increase of 0.5% per year. |

| How are the deductions for health and accident insurance defined? | CHF 4'900 / CHF 9'800 / CHF 1'300 | Deductions are set at CHF 4'900 for a single, widowed, separated or divorced person, and at CHF 9'800 for spouses living in the same household. The amount of CHF 1'300 per child or dependent person remains unchanged, even if the costs of mandatory health care insurance change. |

| How is the value of the Vested Benefits account calculated? | 2.5% | We assume an average annual rate of 2.5% for the change in the value of your vested benefits accounts. |

A question?

A reply within one business day, from a human.